Executive Summary: In an era defined by macroeconomic volatility and elevated interest rate environments, corporate treasury departments are under immense pressure to transition from traditional cash custodians to proactive liquidity optimizers. This comprehensive technical article investigates the critical role of sweep accounts in automating corporate liquidity. By systematically transferring idle cash balances into interest-bearing investment vehicles or utilizing them to pay down revolving credit lines, sweep accounts serve as the bedrock of modern treasury management. We will explore the historical evolution of these financial instruments, dissect their underlying architectural mechanics, provide detailed technical analyses of various sweep structures (including MMMFs, Repo, and Commercial Paper), and examine real-world application scenarios and failure cases. Furthermore, this document provides actionable strategies and explores future trends, such as AI-driven predictive liquidity and blockchain-based intraday sweeps, ensuring corporate treasurers can maximize overnight investment yields while rigorously managing counterparty risk.

1. Introduction: The Evolution of Corporate Liquidity Management

The mandate of the corporate treasurer has undergone a profound transformation over the past three decades. Historically viewed as a back-office administrative function focused primarily on ensuring adequate funding for daily operations and mitigating basic financial risks, treasury management has evolved into a highly strategic, yield-generating epicenter within the modern corporation. At the heart of this transformation is the aggressive optimization of working capital and the deployment of automated liquidity mechanisms, most notably sweep accounts.

1.1 The Historical Context of Idle Cash

Prior to the digital revolution in commercial banking, managing corporate cash was a highly manual, labor-intensive process. Corporate treasurers relied on end-of-day bank statements, physical ledgers, and manual wire transfers to consolidate funds from disparate regional accounts into a centralized concentration account. Because banks required significant time to clear transactions and update balances, a substantial portion of corporate liquidity remained idle—sitting in non-interest-bearing demand deposit accounts (DDAs) overnight or over the weekend. This “cash drag” represented a massive opportunity cost, particularly during the high-inflation, high-interest-rate periods of the late 1970s and 1980s.

Regulatory frameworks also played a pivotal role. In the United States, Regulation Q historically prohibited banks from paying interest on corporate DDAs. To circumvent this regulatory restriction and offer value to corporate clients, commercial banks engineered the first iteration of sweep accounts. By mathematically “sweeping” funds out of the corporate DDA at the close of business and into an off-balance-sheet investment vehicle (such as a repurchase agreement or an offshore branch account), banks allowed corporations to earn interest on their overnight balances without violating Regulation Q. The funds, along with the accrued interest, would then be swept back into the operating account at the opening of the next business day, ensuring total liquidity for daily accounts payable and payroll disbursements.

1.2 The Paradigm Shift to Automated Liquidity

Today, the deployment of sweep accounts is no longer a regulatory workaround but a fundamental component of automated liquidity management. The integration of sophisticated Treasury Management Systems (TMS) and Enterprise Resource Planning (ERP) platforms via Application Programming Interfaces (APIs) has enabled real-time visibility into global cash positions. Consequently, the reliance on manual cash concentration has been entirely replaced by automated rule-based architectures. Modern sweep accounts automatically identify balances exceeding a predetermined threshold (the “target peg”) and route those excess funds into high-yield money market mutual funds (MMMFs), commercial paper, or debt-servicing mechanisms.

Pro Tip for Treasurers: When establishing a sweeping architecture across multiple subsidiaries, transition away from legacy MT940 reporting and leverage ISO 20022 XML formats (such as CAMT.053). The richer data structure of ISO 20022 drastically reduces reconciliation errors when un-sweeping funds back into localized operational accounts.

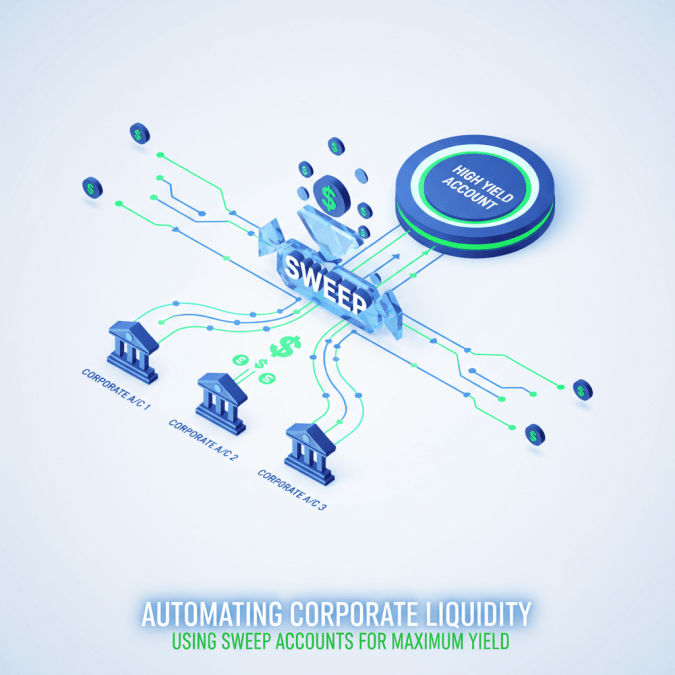

2. Unpacking Sweep Accounts: Mechanics and Architecture

To fully leverage sweep accounts for maximum yield, a thorough technical understanding of their underlying operational mechanics is essential. A sweep account is not a standalone financial product but rather an automated, algorithmic linkage between a primary transactional account (usually a DDA) and a secondary investment or liability-management vehicle.

2.1 Core Mechanisms of Target-Balance Accounts

The foundational principle of a sweep account is the establishment of a “Target Balance” or “Peg Balance.” This is the specific dollar amount that the corporation and the banking institution agree must remain in the DDA at the end of the processing day to cover the next day’s anticipated operational expenses (e.g., checks clearing, ACH debits, wire transfers) and to compensate the bank for account maintenance services via earnings credit rates (ECR).

The daily operational cycle follows a strict, time-bound sequence:

- Intraday Operations: Throughout the business day, the primary DDA receives incoming cash flows (accounts receivable, point-of-sale deposits) and processes outgoing cash flows (vendor payments, payroll).

- End-of-Day (EOD) Cut-off: At a mathematically defined cut-off time (e.g., 4:00 PM EST), the bank’s core processing system takes a snapshot of the DDA’s ledger balance.

- Algorithmic Assessment: The system compares the current ledger balance against the predetermined Target Balance.

- Surplus Scenario: If Ledger Balance > Target Balance, the system initiates a debit for the difference, sweeping the excess funds out of the DDA and into the linked investment vehicle.

- Deficit Scenario: If Ledger Balance < Target Balance, the system initiates a credit, sweeping funds from the investment vehicle (or drawing from a line of credit) back into the DDA to restore the peg.

- Next-Day Reversal (Optional but Common): For certain investment sweeps, the principal and accrued interest are automatically swept back into the DDA at the start of the next business day. Other structures leave the principal in the investment vehicle, only sweeping back what is strictly necessary to maintain the peg.

2.2 Technical Infrastructure and System Integration

The execution of these daily sweeps relies heavily on the bank’s internal ledgering systems and their seamless integration with external clearing houses (like the Federal Reserve Bank’s Fedwire system or the Automated Clearing House network). For corporate treasuries managing a global footprint, a primary DDA in New York might be linked to a master concentration account in London, necessitating cross-border, multi-currency sweep capabilities.

Technically, the bank’s sweeping engine executes batch processing scripts. However, modern corporate infrastructure demands that this activity is mirrored perfectly in the corporate ERP (e.g., SAP, Oracle). The bank must transmit intra-day (CAMT.052) and end-of-day (CAMT.053) statements so that the corporate ledger automatically reconciles the sweep transfer. Failure to establish tight API or Secure File Transfer Protocol (SFTP) integrations results in massive “unreconciled” suspense accounts on the corporate balance sheet, creating audit liabilities.

3. Strategic Imperatives: Why Sweep Accounts Drive Corporate Yield

The commercial investigation into sweep accounts reveals that they are not merely conveniences; they are powerful strategic tools designed to execute three primary financial imperatives: yield maximization, interest expense mitigation, and counterparty risk management.

3.1 Maximizing Overnight Investment Yields

In high-interest-rate environments, the opportunity cost of uninvested cash is staggering. Consider a mid-market enterprise with an average daily idle cash balance of $25 million. If this cash sits in a standard non-interest-bearing DDA, the yield is zero. If the firm utilizes an overnight investment sweep account yielding an annualized rate of 5.15% (tracking closely to the Secured Overnight Financing Rate – SOFR), the automated sweep generates substantial passive income.

Calculation of Overnight Yield:

$25,000,000 × 5.15% = $1,287,500 annualized.

Daily Yield = $1,287,500 / 360 days = ~$3,576 per day.

Over a three-day weekend, that un-swept cash would cost the company over $10,700 in lost revenue. By automating this process, the corporate treasury captures the “compound effect” of daily interest accrual without requiring a human trader to manually execute commercial paper purchases or fixed-term deposits.

3.2 Debt Servicing and Interest Expense Mitigation (Loan Sweeps)

While earning 5% on idle cash is attractive, corporate debt structures often carry much higher interest rates. A revolving credit facility or line of credit (LOC) may carry an interest rate of SOFR + 300 basis points (effectively 8% or higher). In this scenario, earning 5% on an investment sweep while simultaneously paying 8% on a drawn credit line is a mathematically sub-optimal use of corporate liquidity.

To resolve this, treasurers deploy Loan Sweep Accounts (also known as two-way automated sweeps). In a loan sweep architecture, excess cash in the DDA is not invested in a money market fund; instead, it is automatically swept to pay down the principal balance of the corporate line of credit. If the DDA falls below its target balance the next day, the system automatically draws against the LOC to replenish the cash. Because avoiding an 8% interest expense mathematically equates to an 8% risk-free return, loan sweeps are often the most profitable deployment of short-term liquidity for levered companies.

3.3 Enhanced Counterparty Risk Mitigation

Corporate cash balances routinely exceed standard deposit insurance limits (e.g., the $250,000 FDIC limit in the US). If a commercial bank fails—a scenario highlighted by the 2023 collapses of Silicon Valley Bank and Signature Bank—uninsured corporate deposits become unsecured claims in receivership. Sweep accounts mitigate this counterparty credit risk by systematically removing excess funds from the bank’s balance sheet.

By sweeping funds into a Government Money Market Mutual Fund (which holds underlying assets of US Treasuries) or a tri-party repurchase agreement (collateralized by government securities), the corporate entity legally transfers its exposure from the commercial bank’s balance sheet to sovereign-backed instruments or segregated off-balance-sheet vehicles.

3.4 Comparative Matrix of Sweep Structures

| Sweep Structure | Primary Objective | Mechanics | Risk Profile |

|---|---|---|---|

| Investment Sweep (MMMF/Repo) | Yield Generation | Excess DDA funds are swept into high-yielding off-balance sheet money market instruments. | Low. Risk is shifted from bank credit risk to the underlying fund/collateral. |

| Loan Sweep (Revolver) | Interest Expense Reduction | Excess cash pays down principal on a revolving line of credit; deficits trigger auto-drawdowns. | Virtually Zero. Direct reduction of corporate liability; no external investment risk. |

| Zero Balance Account (ZBA) Sweep | Cash Concentration | Subsidiary accounts are swept to exactly $0.00 daily, moving all funds to a master header account. | Internal. Risk remains with the primary banking partner holding the master account. |

| Insured Cash Sweep (ICS) | Deposit Insurance Maximization | Large balances are fragmented and swept into sub-$250k tranches across a massive network of partner banks. | Zero. Maintains 100% FDIC insurance across multi-million dollar balances. |

4. Deep Technical Analysis of Sweep Account Variations

The selection of the destination vehicle for swept funds is a critical decision that requires a nuanced understanding of financial markets, regulatory constraints, and liquidity parameters. Corporate treasurers typically choose from four primary sweep variations.

4.1 Money Market Mutual Fund (MMMF) Sweeps

The most ubiquitous form of corporate investment sweeping involves Money Market Mutual Funds. However, not all MMMFs are created equal. Post-2008 financial crisis regulations (specifically the SEC’s amendments to Rule 2a-7) fundamentally altered the landscape for corporate treasurers.

Government MMMFs: These funds invest at least 99.5% of their total assets in cash, government securities, and/or repurchase agreements that are collateralized fully by government securities. They are permitted to maintain a stable Net Asset Value (NAV) of $1.00 per share, making them the preferred vehicle for corporate sweeps due to principal preservation and lack of accounting volatility.

Prime Institutional MMMFs: These funds invest in corporate commercial paper, certificates of deposit, and other highly rated short-term debt. While they offer a slightly higher yield (the “credit spread”), institutional prime funds are required to float their NAV (VNAV). This introduces accounting complexities for corporate ERP systems, as a swept dollar might be returned the next day as $0.9998 or $1.0002. Furthermore, prime funds are subject to liquidity fees and redemption gates during times of extreme market stress.

Warning on Prime Fund Sweeps: Corporate treasuries utilizing Prime MMMF sweeps must configure their ERP systems to handle Floating NAV (VNAV) accounting. Failure to appropriately capture fractional gains and losses on daily sweeps will result in compounding reconciliation discrepancies and audit violations. Furthermore, reliance on Prime funds limits access to immediate liquidity if the SEC imposes redemption gates during a systemic credit freeze.

4.2 Repurchase Agreement (Repo) Sweeps

For ultra-large-cap corporations, wholesale repurchase agreements provide a highly secure alternative to mutual funds. In a repo sweep, the commercial bank essentially “borrows” the corporation’s excess cash overnight and provides government securities (Treasuries or Agency debt) as collateral. The bank agrees to repurchase the securities the next morning at a slightly higher price, with the difference representing the interest earned.

To mitigate the risk of the bank defaulting overnight, these sweeps are often structured as Tri-Party Repos. A third-party clearing bank acts as an intermediary, ensuring that the collateral pledged by the bank meets the required “haircut” (a margin of safety, e.g., pledging $102 of securities for every $100 swept) and physically separating the assets from the defaulting bank’s estate.

4.3 Commercial Paper Sweep Facilities

Some highly rated financial institutions offer direct commercial paper sweeps. In this scenario, the corporate sweep automatically purchases the overnight commercial paper of the bank’s holding company. While this offers competitive yields, it deeply concentrates counterparty risk. The corporate entity is trading its status as a depositor for the status of an unsecured senior creditor to the bank’s holding company. If the holding company files for bankruptcy, the swept funds are highly vulnerable.

4.4 Eurodollar and Offshore Sweep Structures

Historically, “Eurodollar sweeps” involved moving funds from a US domestic branch to an offshore branch (e.g., Cayman Islands or Bahamas) of the same bank to bypass domestic reserve requirements and earn higher yields. While changes in Federal Reserve policies (such as the elimination of reserve requirements in 2020) and the transition away from LIBOR to SOFR have diminished the regulatory arbitrage of offshore sweeps, multinational corporations still utilize sophisticated cross-border sweeps to centralize liquidity into tax-advantaged or yield-optimized jurisdictions, navigating complex transfer pricing and withholding tax regulations.

5. Data-Driven Insights: Evaluating the Yield vs. Liquidity Trade-off

Implementing a sweep account is an exercise in quantitative optimization. The corporate treasurer must balance the pursuit of yield against the absolute necessity of intraday liquidity and the frictional costs of the sweeping mechanism itself.

5.1 Analyzing Opportunity Costs in High-Interest Rate Environments

The mathematical justification for sweep accounts scales non-linearly with benchmark interest rates. During the Zero Interest Rate Policy (ZIRP) era spanning much of the 2010s, the net yield on sweep accounts was often negligible, sometimes entirely consumed by the bank’s administrative sweep fees (often ranging from $100 to $250 per account per month, plus basis point spreads).

However, as central banks tightened monetary policy, the data shifted dramatically. If the federal funds rate is 5.25%, a conservative Government MMMF sweep might net 5.05% after fund expenses and bank administrative fees. For a corporation maintaining a $10 million daily cash buffer:

- ZIRP Era (0.25% yield, less 0.15% fees = 0.10% net): $10,000,000 × 0.10% = $10,000 annual yield. This barely covers the operational friction of setting up the account.

- High-Rate Era (5.25% yield, less 0.20% fees = 5.05% net): $10,000,000 × 5.05% = $505,000 annual yield. This transforms the treasury department from a cost center into a formidable profit center, adding over half a million dollars directly to the company’s EBITDA.

5.2 The Impact of Cut-off Times on Execution Yields

A critical, often overlooked technical parameter is the Sweep Cut-off Time. Different investment vehicles have different liquidity windows. A bank might offer a Government MMMF sweep with a 4:00 PM cut-off, but an offshore branch sweep might have a 2:00 PM cut-off due to time zone disparities.

If a corporation consistently receives massive wire transfers from international clients at 3:30 PM, selecting the offshore sweep would mean those massive late-day deposits remain un-swept and earn 0% overnight. A data-driven treasury must conduct a rigorous time-series analysis of intraday cash flows. By mapping the volumetric distribution of incoming wires and ACH settlements by the hour, the treasurer can select the sweep vehicle whose cut-off time perfectly aligns with the company’s peak liquidity realization.

6. Real-World Application Scenarios

To contextualize these highly technical architectures, we must examine how modern corporate entities deploy them to solve complex liquidity challenges.

6.1 Scenario A: The Multinational Conglomerate (Cross-border pooling)

The Profile: A global retail conglomerate operating 1,200 stores across North America and Europe. They maintain hundreds of local depository accounts for regional cash collection.

The Solution Architecture: The treasury implements a multi-tiered sweeping hierarchy.

First, they utilize Zero Balance Accounts (ZBAs). At 5:00 PM local time, every single regional store account is automatically swept to exactly $0.00, pushing the day’s cash receipts into a centralized Master Operating Account in New York.

Second, the Master Operating Account is linked to an Insured Cash Sweep (ICS) network for the first $50 million to guarantee FDIC protection, while the remaining $150 million is subjected to an overnight Tri-Party Repo Sweep.

The Outcome: By automating the concentration of funds via ZBAs, the corporate treasury eliminates the need to manual initiate 1,200 wire transfers daily. The secondary sweep ensures that the concentrated $200 million is fully deployed, safely collateralized, and generating maximum overnight yield, all without human intervention.

6.2 Scenario B: The High-Growth Tech Enterprise (Yield vs. Burn Rate)

The Profile: A Series-D technology start-up that just secured $80 million in venture capital funding. They have a high monthly cash burn rate but currently zero debt.

The Solution Architecture: Because the start-up has no debt, a loan sweep is inapplicable. However, keeping $80 million in a single commercial bank DDA is extremely hazardous (as evidenced by tech start-ups caught in recent regional bank failures). The treasurer sets a target peg balance of $5 million in the primary DDA—enough to cover exactly two weeks of payroll and vendor disbursements.

The remaining $75 million is linked to a Government MMMF Sweep. Crucially, they negotiate a one-way sweep with a manual return. The $75 million earns robust interest. As the primary DDA naturally depletes from operational burn, the treasury software triggers an alert when the balance drops below $1 million, prompting a manual authorization to draw $4 million back from the MMMF to restore the peg.

The Outcome: The start-up mitigates catastrophic counterparty risk while extending their financial runway by generating millions in interest income off their un-deployed venture capital.

7. Failure-Case Analysis: When Sweep Accounts Sub-Optimize

Despite their sophisticated automation, sweep accounts are not infallible. Poor architectural design or systemic macroeconomic shocks can transform a yield-generating tool into a severe liability.

7.1 Case Study: The Hidden Cost of Misaligned Target Balances

A common failure point arises from improperly calibrated Target Balances. Consider a mid-sized manufacturing firm that sets an aggressively low peg balance of $10,000 to maximize the amount of funds swept into their 5% MMMF.

On a Tuesday, the firm is unexpectedly hit with a $150,000 ACH debit from a major supplier that cleared faster than projected. Because the peg was only $10,000, the DDA goes into a deep overdraft condition intraday. The bank either rejects the ACH (causing immense reputational damage and vendor late fees) or covers the overdraft, charging an exorbitant intraday overdraft fee of 18% annualized. The penalties and fees incurred in a single day of overdraft completely obliterate the fractional interest earned from the aggressive sweeping over the past six months.

Pro Tip for Treasurers: Implement a dynamic, rather than static, Target Balance. Use statistical variance analysis on historical accounts payable data to establish a peg balance that covers the 95th percentile of unexpected daily outflows.

7.2 System Integration Failures and Reconciliation Errors

Another profound point of failure occurs at the ERP integration layer. If the bank’s API fails to transmit the CAMT.053 end-of-day file, the corporate ERP (e.g., Oracle NetSuite) assumes the cash is still in the DDA. The next morning, treasury analysts, looking at an artificially inflated cash position on their dashboards, might authorize a massive capital expenditure payment. Because the funds are actually locked in a sweep vehicle and haven’t been un-swept due to the integration failure, the payment fails.

“Cash drag” also occurs when API timeouts result in the bank’s algorithmic engine skipping the sweep entirely for a night, leaving tens of millions earning zero interest.

7.3 The 2008 Lehman Catalyst: Breaking the Buck

The most catastrophic failure case in the history of sweep accounts occurred during the 2008 financial crisis. Many corporate sweep accounts were linked to the Reserve Primary Fund, a massive Prime MMMF. When Lehman Brothers collapsed, the commercial paper issued by Lehman—which was held by the Reserve Primary Fund—defaulted. This caused the fund’s NAV to drop below $1.00 (known as “breaking the buck”). Corporate entities that had swept their secure operational cash into this fund overnight woke up to find their principal permanently impaired and their funds completely frozen. This historical trauma is exactly why corporate investment policies now heavily mandate Government MMMFs over Prime MMMFs for sweep architectures.

Liquidity Trap Warning: Never sweep operational cash required for immediate payroll or tax liabilities into any instrument carrying duration risk or credit risk. Even high-grade corporate commercial paper carries non-zero default probabilities. The primary directive of liquidity management is preservation of principal; yield generation is strictly secondary.

8. Future Trends in Liquidity Automation

The landscape of How to Use Sweep Accounts for Better Cash Management is continuously evolving, driven by rapid advancements in financial technology and macroeconomic regulatory shifts. Forward-looking corporate treasuries are actively preparing for the next generation of automated liquidity.

8.1 AI and Predictive Liquidity Sweeping

Currently, Target Balances are generally static or adjusted manually based on seasonal cash flow forecasts. The future of sweeping lies in Machine Learning (ML) and Artificial Intelligence. Next-generation TMS platforms are ingesting millions of rows of historical accounts payable, accounts receivable, and macroeconomic seasonality data to dynamically adjust the sweep peg daily.

For example, an AI algorithm will recognize that next Tuesday coincides with a quarterly corporate tax payment, regional payroll processing, and historical patterns of delayed vendor receipts. The system will autonomously raise the target peg for that specific day from $2M to $12M, ensuring total liquidity, and then immediately drop it back to $2M the following day to maximize yield. This predictive modeling eliminates the “buffer bloat” of keeping too much idle cash on hand “just in case.”

8.2 Blockchain and Tokenized Deposit Sweeps

The traditional banking system operates on batch processing and is constrained by weekend and holiday closures. If cash is swept into a repo on Friday afternoon, it is locked until Monday morning. Distributed Ledger Technology (DLT) is revolutionizing this.

Major institutions are developing blockchain-based liquidity networks (such as JPM Coin). In these environments, corporate cash is converted into tokenized deposits. Because blockchains operate 24/7/365, corporations can execute minute-by-minute, intraday sweeps. If a corporate account receives a $10 million payment at 1:00 PM, those funds can be instantly swept into a tokenized repo, earn interest for exactly three hours, and be swept back out at 4:00 PM to fund an outbound wire. This intraday yield curve represents the bleeding edge of liquidity optimization.

8.3 Real-Time Payments (RTP) and Intraday Sweeps

The global adoption of Real-Time Payment rails (like FedNow in the US, or SEPA Instant in Europe) complicates traditional end-of-day sweep mechanics. When payments clear instantly 24 hours a day, the concept of a “4:00 PM EOD Cut-off” becomes obsolete. Banks are currently engineering “continuous sweep architectures” that evaluate the target peg in real-time, executing micro-sweeps throughout the day to ensure instant liquidity availability without sacrificing yield.

9. Implementation Strategy and Best Practices

For a corporate entity looking to establish or overhaul its sweep account architecture, a rigorous, phased implementation approach is required to guarantee optimal yield generation without introducing systemic operational risk.

Corporate Sweep Implementation Checklist:

- Conduct Liquidity Profiling: Analyze 12 months of historical daily bank balances to calculate average, peak, and trough cash positions. Determine the absolute minimum operational floor.

- Establish the Target Peg: Calculate a statistically sound Target Balance that covers 95% of expected daily outflows plus a 10% safety buffer to avoid overdrafts.

- Select the Sweep Vehicle: Align the investment instrument with corporate risk tolerance. For maximum safety, utilize Government MMMFs or Tri-Party Repo. If heavily leveraged, prioritize two-way Loan Sweeps.

- Analyze Friction Costs: Model the bank’s sweep maintenance fees, wire fees, and fund expense ratios against projected interest income. Ensure the net yield remains highly positive.

- Review Fund Prospectus: Scrutinize the underlying assets of the MMMF. Confirm it maintains a stable $1.00 NAV and has zero exposure to distressed commercial paper or unregulated shadow-banking entities.

- Architect ERP Integration: Map out the exact API or SFTP file flows (CAMT.052 / CAMT.053) between the bank and the corporate TMS/ERP to guarantee zero-touch automated reconciliation.

- Execute Sandbox Testing: Run a “penny test” phase for one week. Sweep minimal amounts to ensure the accounting debits, credits, and interest accrual journal entries perfectly align on the general ledger.

- Implement Continuous Monitoring: Do not set it and forget it. Treasury analysts should review sweep yields, bank fee statements, and target peg adequacy on a monthly basis to adjust to changing macroeconomic environments.

10. Conclusion

In the modern corporate arena, capital inefficiency is a competitive disadvantage. The commercial investigation into automated liquidity mechanisms proves definitively that sweep accounts are no longer optional treasury tools; they are foundational pillars of corporate financial health. By transforming dormant demand deposits into active, yield-generating, or debt-reducing instruments, corporate treasurers can capture immense value, actively contributing to bottom-line profitability while strictly managing counterparty risk. As interest rates fluctuate and technological innovations like AI and blockchain reshape the financial landscape, mastering the intricacies of target balances, sweep mechanics, and continuous liquidity optimization will remain the hallmark of an elite, forward-thinking corporate treasury department.

Discover more from Kurums | Business Intelligence

Subscribe to get the latest posts sent to your email.